(ATF) China is taking aim at moral hazard. A recent run of bond defaults in the onshore credit market is exceptional not for the number of cases or the amounts at stake, but because the issuers in question are all state-owned enterprises (SOEs) and, in a break with the past, authorities haven’t leapt into action with bailouts.

Rates and credit spreads in the onshore market spiked in the immediate wake of the default on 10 November by Yongcheng Coal & Electricity (Yoncol), a mid-sized, state-owned coal producer in central Henan province. Weak sentiment has spread somewhat to the offshore USD bond market, and Yoncol’s case was preceded by a default from state-owned Huachen Automotive Group (a Chinese joint venture partner of BMW) and followed by state-backed chipmaker Tsinghua Unigroup.

As we detailed last year in a white paper on China’s onshore bond market, this particular type of short-term pain is the necessary ingredient for long-term gain. China’s relatively young onshore bond markets have expanded at a blistering pace in the past decade, but moral hazard has been a constant presence as policymakers were quick to orchestrate bailouts for even some poorer quality firms. Such an approach ensures broader stability but complicates the efficiency of the market when it comes to pricing risk and differentiating credit quality.

In the last two years we’ve seen encouraging signs that policymakers have been reining in moral hazard, especially when it comes to privately-owned enterprises (POEs) and also in the country’s sprawling and strategically crucial banking sector. Now, it appears that SOEs are coming into focus.

SOE issuers in the spotlight

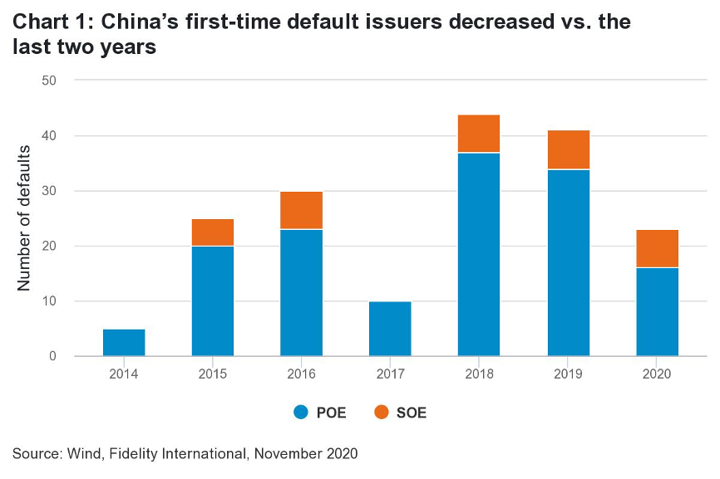

On the whole 2020 has had fewer defaults than the previous two years (Chart 1), so it is not the absolute numbers that matter here. What has rattled investors this time is that these SOEs went into default without much resistance, or forewarning, from policymakers. Moreover, the main shareholders of these entities, generally the provincial governments, did not try to support them financially.

This is fairly unprecedented in China, where the general assumption, rightly or wrongly, has been that the government would step in to help prevent SOEs from defaulting. Bond defaults are still a relatively new development in China’s onshore market: the first corporate bond default was Chaori Solar in 2014, and the first bond default by an SOE was Baoding Tianwei in 2015.

As a result of the recent trio of SOE defaults, the market is scrutinising all weak SOEs’ debt as investors – many of them for the first time – and is being forced to rethink the implicit guarantee on these SOE instruments. Such guarantees are one of the foundations that the sector is built on, especially in the many cases of lower-tier SOEs where standalone credit fundamentals are generally weak.

In Yoncol’s case, authorities have launched inquiries into apparent misappropriation of assets and overstated claims of financial strength. This also shook the market because of the extent to which the creditors’ rights had effectively been deprioritised, including in the weeks leading up to the default, given the involvement of the provincial government in restructuring and asset transfers. The default on principal of a 1-billion-yuan debt was all the more surprising given the company’s most recent financial disclosures. For example, at the end of the third quarter, the company reported cash and equivalents of 33 billion ($5 billion), and even issued a new 1-billion bond on October 22.

More SOE defaults an inevitable growing pain

We think this recent trend of defaults among weaker local SOEs may continue, given China has been tightening monetary policy amid a rebounding economy. It’s all part of the deleveraging process. For example, unemployment has come down from Covid-induced highs in early 2020 but it is still somewhat elevated (see Chart 2).

In the near term, we expect funding costs to remain high while rates stay under pressure due to tightened liquidity. There could be more negative headlines around the SOE sector if local governments remove support for them. Creditors are likely to increase their emphasis on the standalone credit fundamentals, which means spreads will likely widen from historically tight levels, with a bifurcation between stronger and weaker credits of SOEs.

In the long run, a gradually rising number of defaults underpins the development of China’s onshore bond market. This process could improve investors’ visibility on potential outcomes like restructuring timelines and recovery estimates, which will help market participants make more informed decisions. The breaking of moral hazard and stronger precedent of SOE defaults in China are encouraging signs for the more efficient pricing and allocation of capital. All these factors lay the groundwork for more sustainable growth.

# Alvin Cheng, Fixed Income Portfolio Manager at Fidelity International

Fidelity International offers investment solutions and services and retirement expertise to more than 2.5 million customers globally. As a privately-held, purpose-driven company with a 50-year heritage, we think generationally and invest for the long term. Operating in more than 25 locations and with $611.4 billion in total assets, our clients range from central banks, sovereign wealth funds, large corporates, financial institutions, insurers and wealth managers, to private individuals.

Read more at: fidelityinternational.com