(ATF) The Biden administration has wasted no time since taking office to push ahead with its economic support agenda and enacted a nearly $3 trillion spending programme. At the same time US government bond yields have continued to rise, testing the resolve of the Federal Reserve’s commitment to keep rates lower for longer.

Market commentary has focused on the prospect for higher inflation, which was absent after the global financial crisis monetary and fiscal intervention but seems to be a more credible outcome following the outsized level of budgetary and monetary intervention through the Covid pandemic. Bond investors have been willing to position for higher rates in expectation of an economic recovery. Policy in the US remains firmly fixed on government- and central bank-led initiatives to support businesses and individuals ravaged by the economic consequences of the global pandemic, resulting in an expected greater demand for products and services.

Policy initiatives have also been confirmed in China as part of the latest five-year plan, with more of a focus on longer-term strategic goals rather than immediate measures in response to the global pandemic shut down.

Also on ATF

- Vaccines, stimulus boost US jobs

- Trillion dollar man: Biden unveils vast new jobs package

- China boosts factory output as services growth lags behind

Despite the headlines, which promised to boost consumer spending across the board, policies do not target consumption specifically. Instead there is much more of a focus on addressing inequalities between the urban and rural populations. Most of the consumption-led policies have already been in place for a while and tend to be more directed to supply-side initiatives rather than the demand side of the economy.

These promote specific industries and are unlikely to boost household income or the propensity to spend more. As a result, household consumption as a proportion of GDP will increase modestly only. Instead, initiatives aimed at addressing the wealth gap between urban and rural populations, and between the more wealthy and less wealthy take front and centre. The fiscal stance remains conservative. The new plan does however outline significant changes to the household registration system (hukou) and as such could boost consumption in the rural communities. Overall, there is less emphasis on the external sector with the need to develop domestic markets clearly highlighted.

As investors consider the net effects of these two somewhat independent policies pursued by the two global economic juggernauts, news flow continues to highlight similarities rather differences and hence the co-dependencies tend to dominate attention. This will create investment opportunities.

Base effects and the prospect of inflation

China’s Producer Price Inflation (PPI) has increased rapidly as the industrial sector reflates. This is likely to extend further beyond the second quarter, supported by higher oil prices. However the economic growth momentum is expected to peak at the end of the first-half of the year as monetary policy continues to exit from the Covid-inspired easing and curbs on borrowing are set to continue and depress property related activity. In the absence of significant support for demand, most notably investment, it is unlikely that PPI will get ahead of itself and therefore Consumer Price Inflation is likely to remain contained in China.

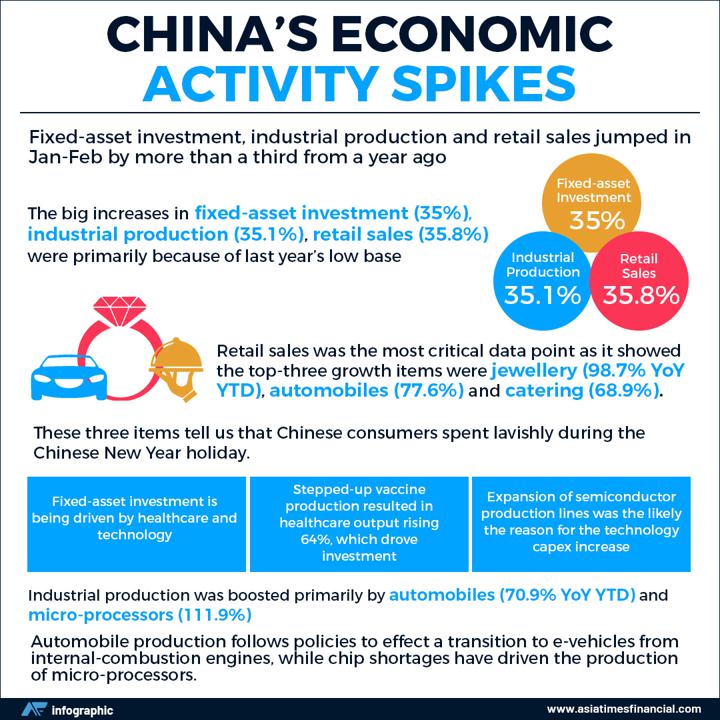

The base effect is distorting the perception of underlying growth in China. The collapse of activity during the onset of the Covid crisis has caused year-on-year comparisons to be exaggerated, including 105% growth in property sales, 64% increase in construction starts and 35% expansion in retail sales. While the Chinese external sector will benefit from US domestic demand support because of the latest round of policy initiatives in the US, growth rates should normalise as we get into the second-half of the year.

Markets are asking the questions in the US

In the US, it is the markets that are asking the questions. Higher breakeven interest rates after adjusting for inflation suggest that consumer prices are set to rise above the 2% target. While this is certainly accommodated by the change in Fed policy management that targets the average inflation rate rather than the peak, it is a test of the Fed’s resolve. Longer-term rates that had moved higher at the end of 2020 have continued to recover the declines of the past two years. This has caused investors to start questioning the outlook for inflation as the economic recovery gains momentum supported by the fiscal programme. Fears that capacity is tight, inventories are low and US households have cash to spend threaten to push rates higher. This has caused a rotation in the equity markets from growth to value and left government bond investors with losses.

Importantly in the US, real yields have not risen by much yet – and Fed policy continues to support real yields. While a modest increase in inflation will continue to favour risk assets including equities over bonds, the risks are rising. However, with existing monetary policy set to continue, it would take a brave investor to bet against the Fed in the next 12-18 months. Talk of a taper tantrum as in 2013 is premature as the US is well committed to its recovery path. Hence, any further momentum in yields is likely to be constrained or short-lived providing traders an opportunity in the short term.

Positioning for the second quarter

Despite the volatility in government bond and equity markets since January, US investment grade credit spreads are trading at the tight end of their recent range. Credit defaults and rating downgrades are likely to stay benign due to significant policy support and a recovering economy in dollar markets. Therefore, the potential for further tightening is limited. Conversely, the pickup in credit spreads across Asian credit markets has remained at the higher end of the range and the shorter duration in these markets will support outperformance.

Investors will do well to stay ahead of the rotation in equity markets as valuations adjust for changing circumstances. While equities remain relatively attractive, the days of the quick and significant recovery are likely gone and investors will have to sweat harder to generate returns.

- Dr Mark Konyn is Group Chief Investment Officer at AIA