The global SPAC boom is over for now. That puts Asian companies that could be sold to existing SPACs in a strong position, but punishes the Singapore and Hong Kong exchanges that hoped to join a listing bonanza

(AF) The boom in special purpose acquisition company (SPAC) launches seen in 2020 and the first quarter of 2021 has slowed.

There are more than 420 existing SPACs still looking for a target, which gives bargaining power to Asian firms that would like to follow Singapore’s Grab, which is merging with a SPAC at a record $40 billion valuation for the sector. This may soon be matched by a deal for a stake in Universal Music by billionaire investor Bill Ackman’s SPAC.

But plans by Singapore Exchange (SGX) and Hong Kong Exchanges and Clearing (HKEX) to exploit a SPAC listing fee bonanza that has been dominated by two giant US exchanges – Nasdaq and the New York Stock Exchange (NYSE) – may now be slow to bear fruit.

Read also: Are SPACs a breeding platform for Asian unicorns?

“There will be some ups and downs along the way, including the relative slowdown in SPAC IPOs we’re seeing now, for a variety of reasons, including some pullback from the stock market run-ups that SPACs had been experiencing, recent pronouncements from the Securities and Exchange Commission and perhaps just a perception that it’s an appropriate time for the SPAC market to catch its breath after the frenetic activity in the first quarter,” said Brian Hecht, a partner at Katten, a US law firm with an office in Shanghai and an active Chinese practice.

SGX launched a proposed regulatory framework for SPAC listings on March 31, with a request for market comments by April 28, in a timeframe that effectively marked the end of the most recent SPAC boom.

SGX is still scheduled to issue concrete proposals for its SPAC regulatory framework soon (it set a target of mid year) but the global SPAC market seems to have settled into a period of sharply lower listing growth and an increased focus on finding merger targets for the many existing vehicles.

Fintech, EV listing

The boom in SPAC listings during 2020 and the first quarter of 2021 marked remarkable growth for a structure that has been around since 1993 but only recently came to play such an important role as the listing approach of choice for many growing companies.

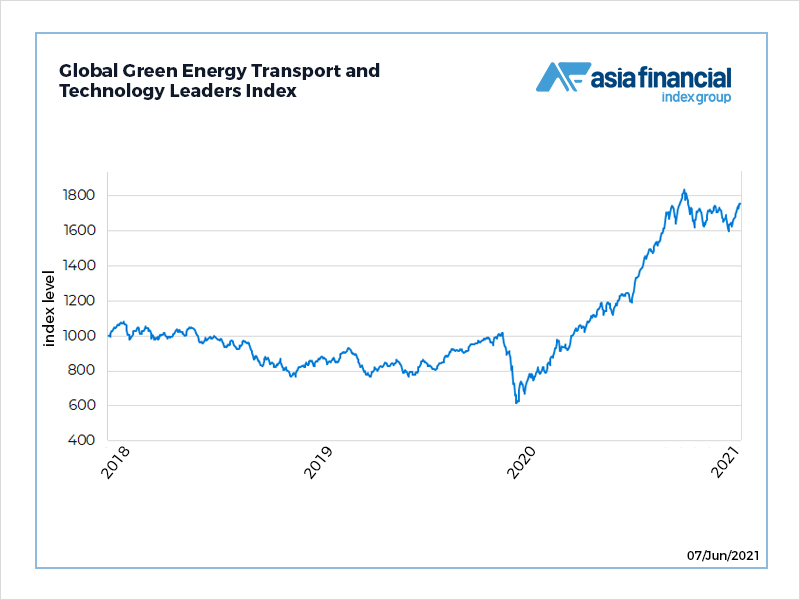

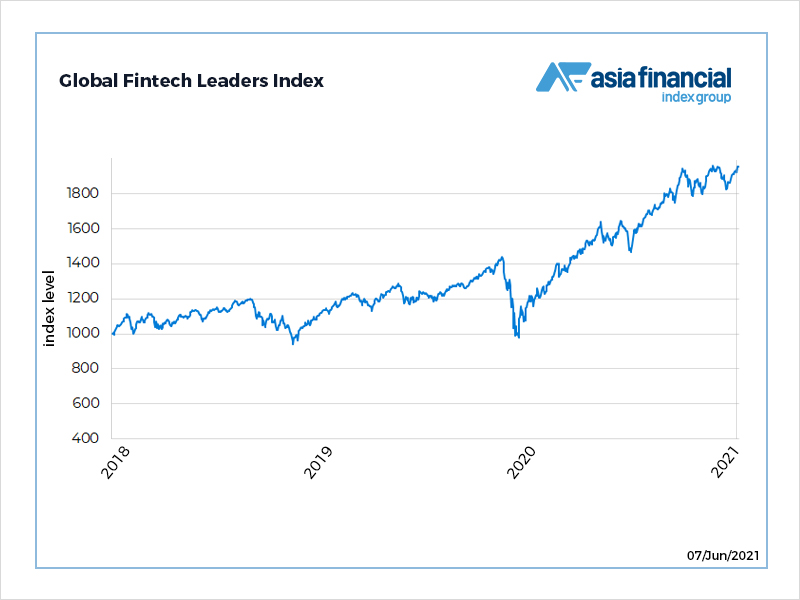

Technology-based companies including fintech firms and electric vehicle (EV) start-ups are among private companies that have been targeted by SPACs. Both the AF Global Fintech Index (KOINTR ) and AF Global EV Index (EKARTR) soared to records this year, echoing surging interest in SPACs.

There were 248 SPAC listings in 2020 for funds raised of $83.3 billion, while 2021 by early June had seen another 330 listings for a total of almost $105 billion, according to data collected by SPACInsider.

But new SPAC listings slowed dramatically after the end of the first quarter of 2021, when 320 of the year’s 330 IPOs by the so-called blank cheque companies came to the market.

There was also a bursting of the bubble in prices for many new and existing SPACs. The structures are by market tradition launched with a $10 value, after which the sponsors of the SPAC normally have two years to find a suitable target for a merger with a private company.

For many years most SPACs traded at or near their $10 value until news that a target had been identified, with prices typically only rising in the approach to a merger announcement, after some inevitable leakage of information into the market.

That changed in 2020 when many SPACs, especially those created by well known investors with a track record of success such as Chamath Palihapitiya or Michael Klein, began to trade at a substantial premium to their nominal $10 value.

Retail interest

Growing appetite for SPAC shares by retail investors helped to drive this premium, which spread to vehicles endorsed by celebrities with no obvious expertise in the sector, such as former basketball star Shaquille O’Neal and tennis legend Serena Williams.

The average SPAC’s premium to its nominal price reached a high of over 25% by early March, in what in retrospect was the recent peak in the pricing bubble. By the end of May the average SPAC premium had disappeared completely and some vehicles were trading below their nominal $10 value.

The slowing in new SPAC issuance and elimination of pricing froth has put the emphasis for the market on the existing vehicles that are searching for merger targets. There were 422 SPACs seeking a target by early June, according to SPACInsider, with a market value of over $130 billion.

That total underestimates the merger firepower of existing SPACs, however, as the recent $40 billion deal for Grab demonstrates. The SPAC Altimeter Growth that will merge with Grab listed with a $450 million IPO last year, and associated Altimeter funds took its total investment to $750 million when the planned merger with the Singapore-based ride-hailing and delivery app firm was announced in April.

But it was the related $4 billion private investment in public equity (PIPE) financing that took Grab’s value to $40 billion ahead of its planned listing in July on Nasdaq with the stock ticker GRAB.

PIPE financing is dominated by large established investors – BlackRock, Abu Dhabi’s Mubadala and Singapore’s Temasek joined the Grab deal – who will play a large role in determining whether the existing 422 SPACs looking to invest before the end of their two year life-spans will be able to secure desirable deals.

The time pressure on these SPACs should give bargaining power to Asian companies that could be merger targets because they are currently still private but offer impressive growth prospects.

Asian advantage

That inevitably brings Asian firms that – like Grab – are reliant on technology into focus.

There was speculation that Indonesia’s two biggest start-ups, ride-hailing firm Gojek and online market Tokopedia, could each be targets for SPACs, for example, before the two firms announced in May that they will be merging to form a new company called GoTo Group and looking for a dual New York and Jakarta listing later this year.

An existing SPAC could still presumably try to tempt the owners of GoTo to merge with it to achieve a listing in New York, but it would have to sweeten any offer if GoTo feels it is on course for a traditional IPO on its own terms.

Asia’s biggest exchanges, led by SGX and HKEX, are likely to press on with plans to change their listing rules to accommodate new SPAC launches.

The exchanges in South Korea and Malaysia that already allow SPACs have seen few listings, however, with only four SPACs coming to market on Korea’s Kosdaq during the boom of the first quarter of 2021.

Asian-based investors such as Hong Kong billionaires Richard Li and Adrian Cheng have used New York to list SPACs that aim to invest in Asian targets, as has Japan’s SoftBank in launches via its Vision Fund.

Likely changes by SGX and HKEX to offer SPAC rules that are in effect slightly tighter than the listing procedures on offer in New York may be slow to yield results, given that the boom in demand for new SPACs seems to have turned to bust for now.

But there are optimists who think the current lull in issuance and deflation in SPAC prices simply represents a pause for the market before a revival of interest.

“It appears, more generally, that the momentum fuelling the SPAC market is sustainable,” said Katten’s Hecht.