(ATF) On the eve of the US Presidential election, Emerging Market bonds play an important role in an investment portfolio. They are leveraged to Chinese and global growth, offer some carry, and have not yet reached pre-pandemic spread levels despite the rally. Emerging Market bonds will be less affected if US Treasury bond yields continue to rise.

It is time to review the case for Emerging Markets, and the November 3 US election is an excellent reason to dig deeper into the investment case for this asset class. Like most asset classes Emerging Markets had a phenomenal rally from April to August. Global monetary stimulus brought corporate yields down, powering bond prices to new highs. But there was always a lingering concern that Developing economies were less well equipped to deal with the health crisis in terms of health infrastructure and financial resources to cushion the economy.

More recently, there has been greater uncertainty around global growth and concerns about the US elections regarding process and outcome. After a very strong growth recovery in the third quarter, some signs of a growth moderation have led to worries about a “mini-W” growth profile. The “W” would be a renewed decline in global growth due to renewed lockdowns.

An uncertain US election was also worrying. In September, investor concerns centered around a contested election, an antagonistic period of recounts lasting a few weeks after election day. These concerns were mitigated as Vice-President Biden managed to maintain his lead of around 9% in nationwide polls and a lead in many “swing states.”

More recently, there were some doubts about the Senate race as it directly impacts the likelihood of a new stimulus package being finally passed.

In the last few days, the increase in Covid case has resurrected fears of renewed lockdowns with their negative impact on growth.

Significant positive factors

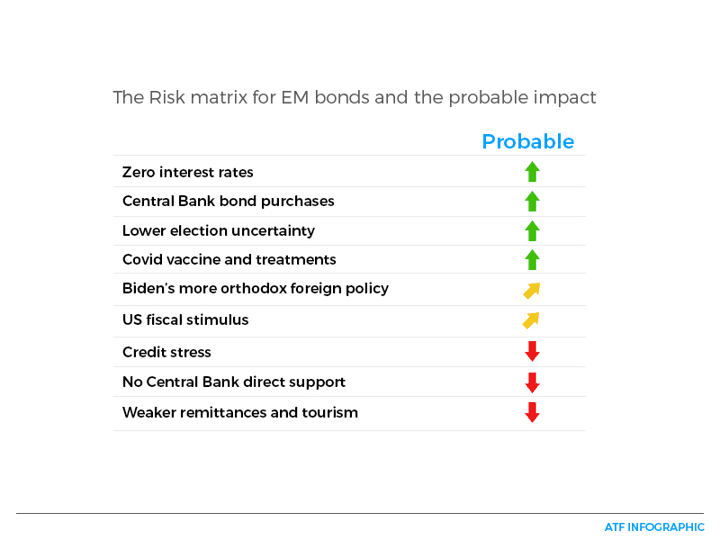

However, there are significant positive factors that support Emerging Market debt. China’s sharp recovery is critical for many Emerging Markets. More robust demand has led to an increase in commodity exports to China and buoyed commodity prices, a significant revenue source for many Developing countries. Going forward, China is likely to continue growing as consumers spend again, and government infrastructure-building programs keep demand healthy.

With policy rates at zero or negative in most developed economies and central banks buying government bonds in many countries, mortgage-backed securities in the US, and lower-rated sovereign debt in Europe, investors are back hunting for yield.

Since the start of the pandemic, central bank balance sheets have grown by over US$3 trillion. While some of the increase in holdings has come from greater government bond issuance, investors also took profits on their government bond holdings and are replacing them with riskier bonds.

In most portfolios, the critical role that government bonds had in stabilising portfolios in times of risk aversion has disappeared. The September sell-off was a good example. The S&P 500 declined by 10%, yet government bonds barely moved. With no yield and no hedging benefits, portfolio constructors are moving out of government bonds. One of their destinations could be Emerging Market bonds, which at least offer positive yields.

The world’s major central banks have all signalled that they would maintain or even increase their asset purchases.

Biden win would be positive for EM bonds

If, as polls suggest, Vice-President Biden wins clearly on November 3, we expect additional positive factors for Emerging Market bonds. US foreign policy will return to a more predictable path. While tensions with China will remain, the uncertainty around “policy by tweet” will end. Greater coordination with other countries will increase and the strategic competition with China could become beneficial for weaker Emerging Markets.

If the Democrats take over the Senate, a large US fiscal stimulus plan could boost the US and global growth. Emerging Markets would then benefit from a recovery in two of the world’s large economies: the US and China.

However, the chance of a “Blue Wave” of Democrat control of the White House and both chambers of Congress is still a toss-up. Investors might even have to wait quite a few weeks until the result for the last of the Senate elections in Georgia is decided.

At current levels, market pricing still leaves more room for upside in Emerging Market bonds, but there are a few risks beyond the US elections. Unlike corporate bonds in Developed Economies, Emerging Market bonds are not part of central bank bond-buying operations and depend more on global investors’ risk appetite. Bond supply has been high: JP Morgan Research estimates that US dollar bond supply in Asia will top $300 billion, beating previous supply peaks of the boom years of 2019 and 2017.

The dismal growth in the first half of this year has led to increased credit stress, which always lags the economic cycle. In some countries, rising poverty and frustration over Covid-19 lockdowns have bubbled into major social unrest. We have seen a sharp sell-off in Chinese real estate bonds, which account for a significant part of Asia’s US dollar issuance this year.

Global travel will take longer to recover, and countries depending on tourism and remittance payments from overseas workers will face ongoing headwinds.

Despite these risks, we expect returns from Emerging Market bonds to contribute to a well-constructed portfolio.

The decline in US policy uncertainty after the election, the potential for a major US fiscal stimulus and the ongoing economic recovery in China will support growth. The discovery and roll-out of a vaccine and better treatments for Covid-19 will address the crisis’s underlying cause.

By 2021, the higher yields of Emerging Market bonds will be irresistible to global investors.

# Rajeev De Mello is an experienced bond investor and chief investment officer based in Singapore. He was Chief Investment Officer for Bank of Singapore and head of fixed income for the Asian operations of various global asset managers. He now runs his own consultancy firm, Deep Learning Investments.