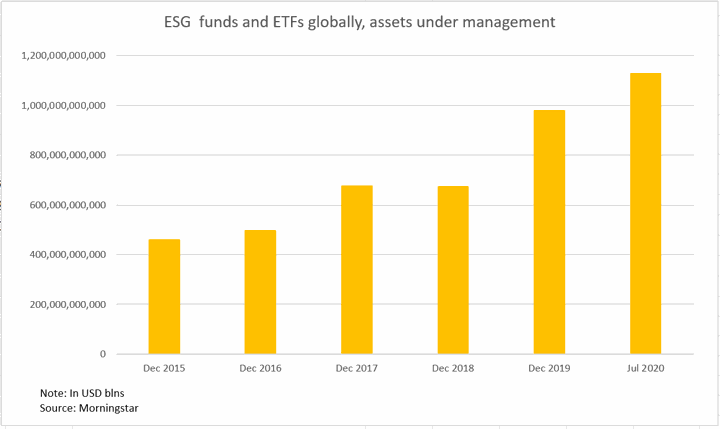

(ATF) It wasn’t so very long ago – no more than three years or thereabouts – that the emergence of environmental, social and governance (ESG) factors as crucial inputs within the international investment arena was described as representing a “quiet revolution.” Not so anymore.

As was confirmed in a digital symposium held by the United Nations-supported Principles for Responsible Investment (PRI) last week, that revolution is no longer rightly characterised as quiet. Very loud and getting louder would be the correct description.

And this applies within Asia-Pacific, the area of focus of the symposium, which featured participants from the financial regulation, asset management and advisory communities.

Confirmation that the rise of ESG within Asia-Pacific is swift moving and shaping up to be a force that companies and asset managers ignore at their peril represents a sea-change for a region that was widely regarded as being a laggard versus the powerful dynamic displayed in Europe and in North America – at state government and asset-manager level, albeit absent the engagement of the Trump administration.

CHINA ENVIRONMENT: Xi’s climate gamble

In terms of regulation, disclosure and taxonomies are the basic inputs. Corporate disclosure of activities within the real economy related to climate change and physical risks is moving from a voluntary to a mandatory regime within APAC and as regulation becomes ever stricter, companies face discrete risks in the form of a curtailment of basic activities and stranded assets – specifically those operating within the fossil fuel complex.

But it’s not all about the environment and climate change: the “S” and “G” aspects are key components, in the case of the former, brought into focus by the Covid-19 pandemic, wherein governments, companies and banks have stepped up to provide crucial aid and financial buffers to address the social impact of the viral onslaught; whilst where it comes to governance inputs such as issues as stewardship on the part of universal asset owners, board composition, proxy voting and gender equality are crucial aspects of ESG materiality.

Green finance and the products therein present another layer such that a box marked “green”can be ticked for example by a domestic investor in China for a bond issued onshore but not for the same product by a foreign investor based, say, in Norway.

The aspiration is that the regulatory environment will move as far as possible towards a global standard based on the strictures of sustainability goals – much as was achieved in 2000 by the introduction of the IFRS standards for corporate accounting.

The grumble remains that there is too much “noise in the system” which interferes with the ability of companies to operate sustainably and for asset managers to make decisions based on the same; data is inconsistent, incomplete and incompatible, and taxonomies – which define what is sustainable – are not harmonised across countries.

As Ashley Alder CEO of the Hong Kong Securities and Futures Commission noted during the symposium, a global green finance taxonomy is still a long way off and the system as it stands allows for the misuse of ESG ratings and scores, with companies at liberty to pick and choose, in the process allowing for “greenwashing” to be widespread.

And he noted the relative lack of a forward-looking modus operandi, which will surely prove to be at the core of the loud ESG revolution that is fast unfurling – as opposed to the “snapshot” approach, which has been the bedrock of accounting and credit analysis since the inception of those industries many decades ago.

Chart: Reuters

As Fiona Reynolds CEO of the London-based PRI noted at her opening address to the symposium: “We need to think not just about what is financially material today, but what is financially material tomorrow and the question of how we can incorporate both material risk and sustainability outcomes into our investment processes.”

Interestingly it was this future-focused mindset imposed by the IFRS on banks’ treatment of loans and expected loss projection, which caused a frisson of balance-sheet adjustment in the sector early last year.

The requirement for banks to set aside capital based on scenario analysis has become a crucial component of the rising prudential stress-testing regimes within the banking sector, which are fast emerging at the behest of central banks and financial regulators globally.

Sustainability criteria will become critical to this process as more and more countries set 2050 targets for zero greenhouse gas emissions in line with the Paris COP 21 agreement to limit global warming.

Carbon pricing policy

But crucial input elements are missing or insufficient – there is an absence of a carbon pricing policy and too much information is qualitative rather than quantitative. The former is critical within APAC where around 40% of electricity production is coal-based.

Singapore has been moving fast on the carbon front – a common tax on emissions is in place alongside a policy to restrict the annual growth of cars and motorbikes to 0%.

And the country’s green action plan, which aims for the transition to a circular, zero-waste economy, envisages that the city-state will become a green finance hub, based on financial technology leverage.

The “G” element within ESG has been a driver of regulation in India, a country that‘s earned a reputation for sharp corporate practice over the years, which helps explain the mass of toxic debt sitting on the country’s struggling banks’ balance sheets, containing new lending in the process: stewardship codes became mandatory last year, appropriate given the surge in mutual-fund assets within the country – from $184 billion in 2015 to $330bn this year, much of those assets under management on the books of state-owned entities.

Systemic abuses in the form of related party transactions instituted by owners and promoters have plummeted as the result of increased e-voting by mutual funds, while mandatory requirements have increased the number of female members on the boards of Indian companies.

China improves

Meanwhile, China is fast moving to become an ESG cheerleader and the number of signatories to the PRI within the country – the growth of PRI membership is regarded as a benchmark for the pace and depth of the ESG “revolution” – has been rising apace.

In China’s case the issue of a sustainability taxonomy and its application both to the real economy and to green finance is apposite. Questions hover over the intentions of China’s government with regard to sustainability and climate change.

Whether the aim is to make “brown” infrastructure more green through such mechanisms as carbon capture – and in the process reduce the lethal pollution that has often blanketed the country’s manufacturing hubs – or to commit to zero emissions is a moot point, particularly given the country’s ongoing investment in coal-fired electricity production. All the more so given the ongoing construction of China’s vast continent-crossing Belt and Road Initiative infrastructure project.

CHINA MINING: China’s exports of vital rare earths drop 62%

But it seems that China is starting to tick the ESG boxes. A national plan to boost the green financial system was initiated a few years ago and banks have been providing more green credit. The country has recently instituted a mandatory ESG reporting regime and has unveiled a Green Bond Catalogue, a taxonomy covering such products issued within the country.

That move is significant. While almost all of the green-bond issuance brought by Chinese entities offshore in recent years has complied with the Green Bond Principles of the International Capital Markets Association (ICMA), the same cannot be said for onshore issuance.

But as the Chinese financial authorities begin the process of opening up the country’s domestic debt market to offshore participation – international credit agencies such as S&P and Fitch are now rating Chinese debt and foreign financial institutions such as BNP Paribas, Deutsche Bank and Standard Chartered are able to lead-underwrite bond deals onshore –the need to meet international standards is pressing.

This all the more so as foreign capital flows are rising thanks to the ease of utilising the Bond Connect platform and the dynamic underpinned by the inclusion of Chinese debt within international bond indices.

The Chinese domestic green bond market almost represents an asset class in search of willing buyers – the sustainable bond fund in Norway, for example, whose asset managers just need the necessary boxes to be ticked in terms of compliance with international norms to have license to start buying.

Explosive growth in green-bond issuance from China – which already sits at number two in terms of global green bond issuance – underpinned by foreign fund participation beckons.

Panda Bonds

It seems reasonable to assume the dynamic will kick off in the Panda Bond market, wherein foreign banks will bring to bear international green strictures for their clients, and where issuance this year is already on target to outstrip last year‘s almost $6bn tally.

Governance is also a key issue in China – as Katherine Han of Harvest Fund Management observed during the PRI symposium, of the over 100 cases of bond default researched by the fund, most involved cases of malfeasance in the face of weak internal controls.

In time, if the loud ESG revolution continues, it’s conceivable that ESG ratings will supplant traditional credit ratings as the materiality of ESG risk looms ever larger.

There exists room to arbitrage credit ratings and ESG ratings within the fixed income asset class – that arbitrage opportunity should vanish as the credit proposition of an entity becomes more and more forward looking and intertwined with ESG considerations such as material, reputational, physical and policy risk.

It might be tempting to imagine, as was the case until fairly recently, that the rise of ESG is a fad that will vanish in the face of the ascendancy of hard-nosed capitalism. But somehow I don’t believe the asset management community will be saying with a collective smile in a decade or so “Remember the days when it was all about ESG? Whatever happened to that?”

Some revolutions change the system for good. This is one of them.