Investors had no place to hide as stock and bond markets tanked simultaneously for the first time since the 1980s, when markets offered no hedges against collapsing values.

In 2008, bond prices rose sharply as stock markets crashed. Now bonds offer no refuge against collapsing stock prices. The difference is that total US public debt outstanding has risen from about $9 trillion at the beginning of 2008 to $23.5 trillion today.

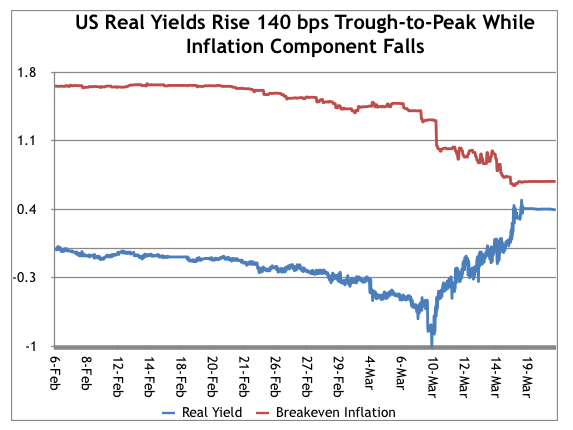

With equities down nearly 6% in Europe and US markets poised to open with similar losses, European bond yields soared and US bond yields rose, as governments prepared trillions of dollars of new debt financing to support economic stimulus and market bailout programs. Between March 9 and this morning, so-called real yields, that is, the yield on inflation-protected US government securities, had risen from a trough of negative 1% to positive 0.4%, the fastest yield spike in market history.

German real yields meanwhile rose by 80 basis points during the same period. Italian real yields meanwhile rose by more than 160 basis points, the worst among the world’s bond market, as Italy remained locked down under health emergency measures.

The market has set a limit to how much money governments can spend to indemnify the world economy against a global freeze-up of activity. President Donald Trump’s proposed trillion-dollar stimulus program announced yesterday afternoon did not impress markets. If the Administration had acted weeks ago, as I proposed, a smaller stimulus program might have restored confidence. Now investors think that governments are chasing after a market that has already started to roll downhill.

Yesterday European central banks spent $130 billion in money borrowed from the US Federal Reserve to replenish liquidity in European banks. As I reported last week, European and Japanese banks were unable to renew credit lines from their US counterparts, which in turn are facing a run on credit lines from their American customers. That forced foreign banks and institutional investors to sell safe dollar assets, including government-guaranteed mortgage backed securities. The central banks succeeded in stabilizing the interbank funding market, and the mortgage-backed securities market has begun to stabilize.

But credit markets continue to freeze up. The cost of credit protection for an index of high-yield bonds soared from +2.8% above the interbank rate in mid-February to 7.25% today. Citibank’s subordinated debt now costs more than 2% to protect, vs 0.4% in February. And investors who want to protect against default on Deutsche Bank’s subordinated debt pay more than 6%, the worst since the 2008 crisis.

Before the present crisis, the US government was running a deficit of more than $1 trillion, or over 4% of GDP, an extraordinarily high level at a time of full employment. The proposed stimulus measure will more than double the deficit, not including the nearly trillion dollars that the Federal Reserve is committed to spend to support the Treasury market, the interbank lending market, and – possibly -municipal and other bond markets.

For the first time since the US Civil War, the credit of the United States is in play.