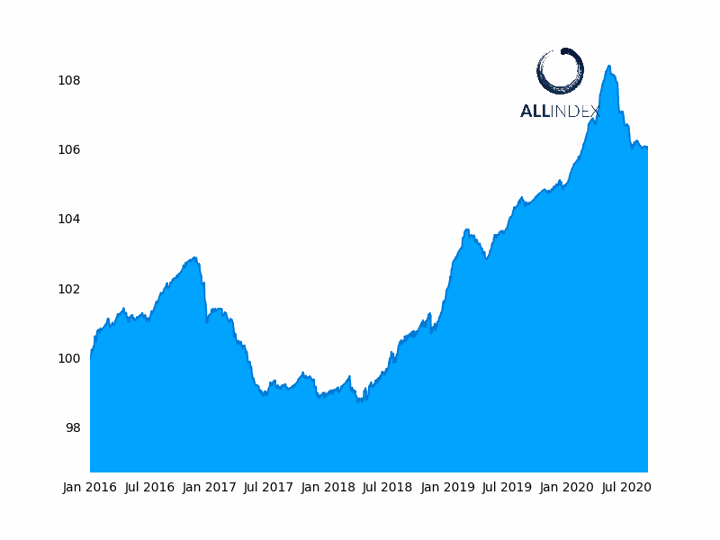

(ATF) The flagship China Bond 50 and ATF ALLINDEX Financial gauges retreated on Friday, with losses in the bonds of financial institutions dragging down the indices ahead of a busy data week.

Retreats were seen in the bonds of Citic Securities (0.62%), China Merchants Bank (0.64%), Agricultural Bank of China (0.23%), Bank of Communications (-0.17%) and Shanghai Pudong Development Bank (-0.04%). The China Bond 50 index fell 0.02%, while the ATF ALLINDEX Financial dropped 0.04%.

The other ATF indices posted smaller moves, with the ATF ALLINDEX Corporates closing down 0.01%, and the ATF ALLINDEX Enterprise not moving at all. The ATF ALLINDEX Local Governments inched up 0.01%.

Export-Import Bank of China, a constituent of the China Bond 50 index, recorded the biggest gains of the day across all the indexes, climbing 0.38%.

ASIAN MARKETS: Fall of rally leading tech stocks slams sentiment

China is due to release its August figures on trade, foreign reserves, inflation and credit growth next week. The market will be watching closely for signs of the country’s continued economic recovery.

“Exports are back in play to be the key driver for Asia’s biggest economy,” Prash Sakpal, senior economist Asia at ING, wrote in a research note.

China’s monthly exports hit $237.6 billion in July, which was just under its December 2019 record of $238.3bn, and could reach $249bn if ING’s forecast of a 16% year-on-year rise for August materialises.

“The persistently large trade surplus and hot money inflows in the global risk-on rally in August should shore up foreign reserves,” stated Sakpal. “Inflation should remain subdued and monetary data should underscore continued accommodative policy.”

Benchmark bond

China’s 10-year government bond yield has rebounded to 3.1% on the back of open market operations by the People’s Bank of China (PBoC) to guide interest rates up and to discourage financial arbitrage. Yields, which sank in early Q2, have now risen to levels similar to those recorded early in the year.

Given that the economy has recovered faster than expected, it is likely that the PBoC will now focus on economic stability rather than growth stimulus, according to Shuncheng Zhang, associate director of China corporate research, Fitch Ratings.

The China Bond 50 Index fell 0.02%

“The PBoC would also want to preserve some policy space for easing in future in case the economy experiences another negative shock,” he said, adding that the central bank has stated that it wants to ensure a “flexible and targeted” monetary policy, and abundant liquidity.

“We do not expect any significant monetary easing in the second half to drive onshore market rates down, unless the economy suffers another severe leg down in the wake of a massive second wave of infections.”

Zhang noted that total onshore corporate board issuance reached a record high of 8.3 trillion yuan ($1.21 trillion) in the first month of the year as result of broad liquidity easing combined with a relaxation of issuance regulation in response to the Covid-19 pandemic. This amounts to 3.3 trillion yuan ($480 bn) in net issuance, which is total issuance minus maturities and redemptions.

State-owned enterprises, which include local government financing vehicles, dominated onshore net issuance, but privately-owned enterprise (POE) issuance nonetheless reached 229.4 billion yuan ($33.53 billion) for the same period. Domestically-rated AAA or AA+ corporates constituted 80% of total net issuance, added Zhang.

However, investor appetite for POEs continues to be weak, especially for those rated lower than AAA.

“This can be underscored by the structural imbalance between SOE’s and POE’s access to the bond market and the dominance of AAA-rated POEs, typically large industry leaders, in POE’s net issuance in the first eight months of the year.”

Furthermore, new asset management rules announced by the People’s Bank of China and due to take effect at the end of 2020 now require bank wealth management products, which used to be large local buyers of lower-rated paper, to be priced based on market valuation of the underlying securities, said Zhang. “This has reduced those products’ appetite for lower-rated, riskier bonds with higher potential market volatility in favour of higher-rated bonds, especially SOE bonds.”