The coronavirus pandemic has created uncertainty for citizens and businesses, and recent research in Hong Kong and Singapore shows it has made people more cautious about what they do with their money and that more have become concerned about their retirement goals

The Covid-19 pandemic has not only destabilised economies and industries around the world, but has also altered our everyday lives. Compared to 12 months ago, many of us work differently, save differently and certainly spend differently.

While the pandemic has created hardship and uncertainty for many, recent research undertaken by St James’s Place* reveals there have been some positive changes in our approach to financial management too.

According to this research, people in Hong Kong are now increasingly cautious with their money, have upped their monthly savings, are more interested in investing in ESG – the environment and social and governance issues – and are more concerned about planning for their long-term retirement goals than 12 months ago.

Such changes, if they continue, could build greater societal resilience as we look towards recovery, and a more positive market outlook in the next six to 12 months.

On the bright side

Over the past year, with hospitality venues, gyms, hairdressers and retail outlets closed and severe restrictions on overseas travel, almost one in two people in Hong Kong (48%) increased their monthly savings. This figure was driven not only by reduced spending opportunities but is likely also due to concerns over job security. Supporting these general feelings of uncertainty, two thirds (60%) of Hong Kongers are now more cautious with money than a year prior.

Such figures reveal how significantly the pandemic has impacted savings habits. While Hong Kong has generally done well at containing the virus, many people are not only trying to reduce expenses but also being more watchful over their finances.

It is therefore no surprise that seven in 10 Hong Kong people are prioritising growing alternative sources of income for themselves most likely in an attempt to make their money work harder and possibly future proof their finances. In addition, there is a clear desire for people to seek out ‘safer’ less risky assets. However, it is worth noting that there are dangers around holding cash with the looming prospect of inflation.

While this increased savings trend could continue and set Hong Kong people up for a brighter financial future, care does need to be taken to ensure people continue to save and invest wisely once vaccines are widely distributed and health risks subside. Given this, it’s vital that people seek appropriate advice to guide them to ensure they make the most of the money they have been able to set aside. Sorting through finances can be complicated and as hard as we try to be rational, there is a level of emotion which can hamper decisions especially during the current stressful circumstances.

Back to the future

However, rethinking retirement planning is something many of us are having to do as our pension savings and retirement income have been impacted by the Covid-19 pandemic. A fact supported by our research that shows 70% of Hong Kong people being currently more concerned about planning for retirement as a result of the pandemic.

Worryingly, slightly more than one in every two Hong Konger’s (51%) has had to draw down or reduce contributions to retirement savings over the past 12 months, with 14% having to do this in a significant way. Essentially, this means many of us will need to work longer and retire later. It could also mean we need to make sacrifices in our retirement, such as selling the family home or adjusting our lifestyle, including reduced leisure and travel activities, to suit our reduced future income.

Unfortunately, it was the younger generation, those aged between 25 and 34, who generally have paid least attention to their retirement savings, and who made the most drawdowns and reductions in contributions. Essentially it means that our young people are ‘kicking the can down the road’, using their future money to pay for current living expenses, and in effect losing the most from decades of foregone returns.

For those young people who are still employed, now is the time to take advantage of any savings made through living with family, reduced spending on travel and going out, and aim to put the surplus into savings plans or pension funds.

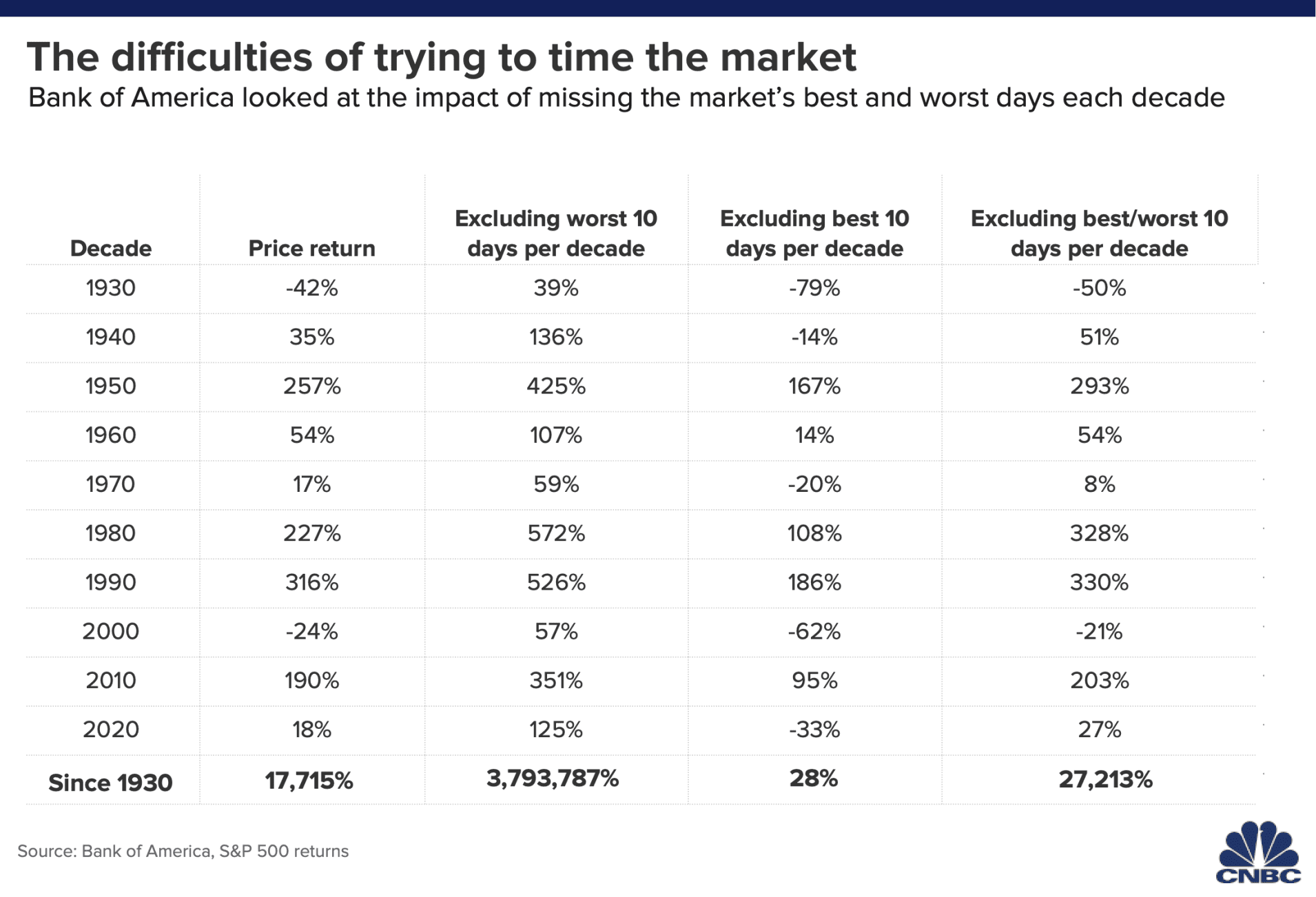

Most importantly, the old investor’s adage, that time in the market matters much more than trying to time the market, holds true. Data from the S&P 500 shows that if investors had excluded only the ten best days of the last decade, they would be sitting at a loss of 33%, compared to a return of 18% if they had stay invested throughout. Amid painful initial shocks and a rocky recovery, the pandemic will hopefully serve as an important lesson for many younger investors that it’s never that bad.

Appetite for advice

Despite the focus on saving and looking at longer term financial goals, most Hong Kong people are turning to family (66%) and friends (38%) for financial advice, as opposed to an independent financial adviser (37%).

Seeking financial advice about how to achieve long-term financial goals is key to making the most of what people have been able to accumulate during this time, something that seven in 10 people (69%) are considering according to this study. However only two in five (41%) currently engage a financial adviser. And while there is also greater acceptance of online advice (31%), more than two thirds of the respondents in this study reported that face-to-face financial advice is important.

It is somewhat ironic that only during a full-blown pandemic where distancing is required, that the true value of financial advice is realised. Family and friends will always remain an important source of counsel but given the current uncertainty globally, the new world of wealth will also herald a new age for financial advisers, who will be sought out in much greater numbers for their experience, guidance but also impartiality. Many will appreciate the need for a voice of reason to guide against fear, bias or greed.

Given the current uncertainty in the world, there is clearly a need for wealth advisers to help people focus on making the ‘right’ financial choices. Whether it comes to investing in alternatives, ESG, long-term savings goals or planning for retirement, independent financial advisers can help to ensure people make the most of the money they have accumulated and also help those to get back on track if they have had to dip into their savings during this time.

*Research by St James’s Place, titled ‘The New World of Wealth 2021’ is an independent study which looks at the impact of the Covid-19 pandemic on wealth management habits and financial advice trends for Asia. A total of 2,017 interviews were conducted online in February and March 2021 in Hong Kong (1,012) and Singapore (1,005).

{kind=link}