(ATF) China’s colossal stimulus plan – unveiled at its annual gathering of parliament – has also boosted bond investors, who say issuance will be gradual and well supported by central bank measures.

The world’s second largest economy is targeting a budget deficit of 3.76 trillion yuan and together with the announced special central government bond issuance of 1 trillion yuan and special local government bond issuance of 3.75 trillion, it would imply a net bond supply of 8.51 trillion this year, a 78% increase over 2019’s net supply of 4.79 trillion, according to DBS estimates.

But this monster supply is expected to be easily absorbed by the market.

“Given the supply and continued inflows from foreign investors, we continue to have a constructive view on China onshore rates, particularly given the higher yield when compared to other government bonds and low correlation benefits with other key asset classes,” Vanessa Chan, Investment Director at Fidelity International, said.

The timing of the supply was also likely to be gradual, allowing the market plenty of breathing room.

“The impact on the bond market should be limited and temporary. It is likely the 1 trillion special treasury bond issuance will be split into several episodes and the central bank still has policy tools such as cuts on required reserve ratios to keep ample market liquidity,” Shuncheng Zhang, associate director of China Corporate Research at Fitch Ratings, said.

Sell-off likely temporary

Deutsche’s Asia Macro strategist Sameer Goel said: “We see the recent sell-off as more driven by position adjustment, and exaggerated by illiquidity, though also in part disappointment with the policy stance continuing to be more selective in its easing rather than being broad-based. We feel supply risk has been largely priced in at these levels. We are recommending 2Y CDBs on an asset swapped basis.”

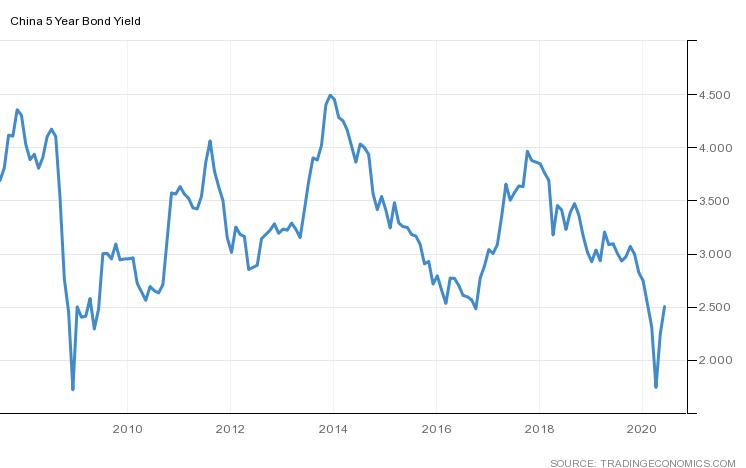

Since hitting an 11-1/2 year low of 1.74% in April, China’s 5-year government bond yields have jumped to 2.5% triggering a scramble from PBoC to inject liquidity into the system.

In a bid to ease the tightness, the central bank injected 120 billion yuan ($17 billion) on Monday, on the back of 150 billion yuan on Friday. It had added 70 billion yuan on Thursday also.

RRR cuts expected

And to keep the environment accommodative, Nomura expects the PBoC to cut the RRR by 100bp before end-September, and to deliver another 50bp RRR cut in Q4.

“June is usually a volatile month anyway for interbank liquidity, as it’s end-H1, so uncertainties over next monetary policy move may be exacerbating this liquidity driven move,” said Jinny Yan, Chief China Economist at ICBC Standard Bank.

“Excluding the special CGB, official fiscal budget and special bonds together make 7.5% of GDP, which appears to be modest if compared with many western economies (10% – 20% of GDP in some cases),” she added.

The demand dynamics are also good.

Ongoing inclusion processes for GBI-EM and BBGA indices should ensure stable passive monthly inflows of around 6 billion yuan, according to DBS Bank strategist Duncan Tan.

“FTSE Russell is also considering CGBs for inclusion into the WGBI index and a positive decision could come at the September review,” he said.

But key to the market stabilising is liquidity at commercial banks, which are still the dominant investor group.

“More required reserves ratio (RRR) cuts would be key to unlocking liquidity that banks could then use to absorb more of the higher CGB supply,” DBS’s Tan said while adding that given the weighted average RRR for banks is at 9.4% and the all-time low was 6% in early 2000s, so there was much room for more RRR cuts.

“Importantly, banks should find it attractive to park the released liquidity in CGBs. The year to date 30bp cut to reverse repo rate and 37bp cut to interest paid on excess reserves have resulted in wide spreads of CGB yields vs funding costs.”