Although investor optimism on the global economic recovery remains high, it is important not to underplay the economic risk from a resurgence in Covid-19 infections

The global economy looks set to enjoy strong growth in 2021, with the momentum going into 2022. Vaccinations are being administered across countries, albeit more effectively in the developed economies.

In the US, the pace of vaccination appears to be proceeding steadily. Coupled with the very substantial fiscal stimulus already in the economy, US gross domestic product (GDP) is likely to surpass 6%, above its 1.5-2% long-term GDP growth rate. The $900 billion Consolidated Appropriation Act and the US$1.9 trillion American Rescue Plan Act 2021 would further boost household income significantly.

Meanwhile, the improving jobs market means that the US consumers’ willingness to spend would potentially increase in the months ahead. Hence, we will probably experience a period of “US exceptionalism” with the country’s GDP growth very likely exceeding the rest of the world.

Asia, including China, in contrast has been conservative in their fiscal stimulus measures. To date, China has recovered well from the Covid-19 pandemic and the authorities are circumspect about pump-priming the economy, preferring to be prudent about leverage and return the country to a path of debt consolidation.

The Covid-19 situation threatens to dampen growth in Asia where the emergence of Covid-19 variants and new infections dim hopes of economic re-opening. Although global growth outlook remains positive, investors should monitor and assess the evolving situation closely given high investor optimism on global growth.

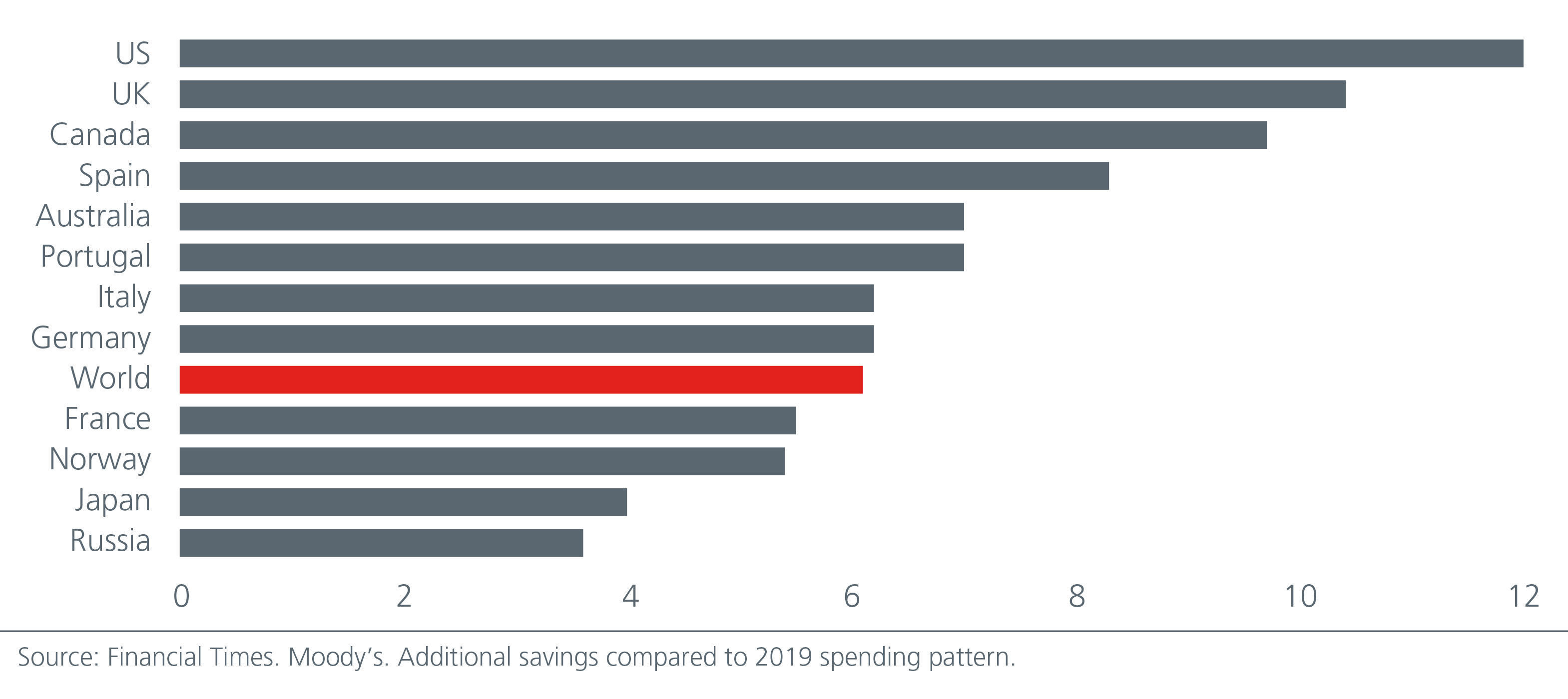

Fig. 1. Excess savings as % of GDP (estimated)

Apart from the substantial fiscal stimulus boosting the US economy, US exceptionalism is also dependent on the Federal Reserve maintaining a loose monetary policy. The Fed currently has a benign view of long-term inflation and sees the need for policy patience until US growth is on a solid footing and inflation runs sustainably higher.

With Asian governments clearly much more conservative in their fiscal stimulus measures, it is unlikely that Asian central banks will tighten policy ahead of the Fed. This means that Asian equity and credit markets should be underpinned by the prospect of low interest rates and supportive asset purchases.

The outlook for the US dollar is less clear, although the more obvious argument is that the greenback should be supported by the US’ stronger growth prospects. However, optimism over the US economy is already largely factored into asset prices. The Fed would not be raising rates for a while.

TWIN DEFICITS

In addition, the significant fiscal stimulus has caused the US twin deficits to deteriorate. On balance, the dollar is likely to stay rangebound in the near-term, but select Asian currencies should resume their appreciation against the greenback in the medium term. In the next three to six months, the Chinese yuan, Korean won and the Singapore dollar are looking positive.

The US is preferred to broad emerging markets (EMs) as Covid-19 developments continue to play out and the likes of India and Latin America struggle to cope. There is also the increasing threat of higher interest rates that would disproportionately impact the more vulnerable EMs.

Accommodative monetary and fiscal policy remain in place and are crucial pillars of support to asset markets. Fiscal stimulus which includes direct cash injections to the consumer is elevating household disposable income and should boost consumer spending. This underlying demand is set to remain strong with companies reporting better-than-expected earnings.

This backdrop for risk assets leads us to favour high yields over investment grade debt but does not augur well for sovereign bonds. Inflation is not an immediate cause of concern given that the recent rise has been driven by transient reopening factors and a rise in metal and oil prices, both of which may not indicate sustainable trends.

Nevertheless, it has the potential to become a structural problem later down the road, particularly if supply bottlenecks sustain. Among equity sectors, those that benefit from a cyclical recovery such as financials, industrials and materials are favoured.

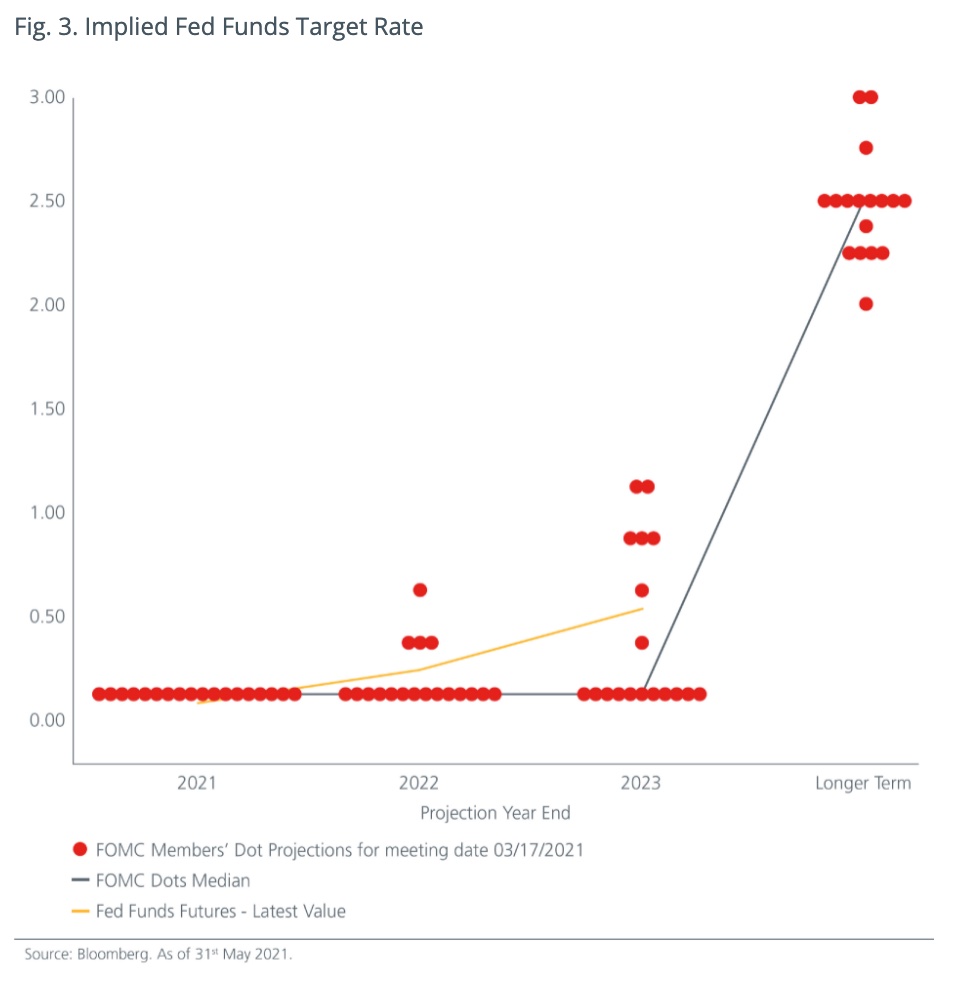

The market has priced in a 25-basis point (bp) rate increase by late 2022 and a further 25 bp by end 2023. This pricing is by no means very aggressive although it is more than the “do nothing” stance which the Fed has expressed through 2023. We believe that the Fed may tighten once in 2023. While the Fed has expressed increasing confidence over the economic outlook, it also wants to meet its full employment and inflation goals.

Meanwhile, labour market slack in the US remains high. With the Fed’s average inflation targeting framework, 2020’s low inflation gives the Fed room to remain dovish. Recent US inflation data has moved up quite sharply partly due to base effects. The Fed will continue to monitor the price pressure developments going forward and will need more time to confirm that most of the increases in prices are indeed transitory.

Any unwinding of the market’s Fed rate rise expectations would likely come from disappointments over global growth, either from renewed economic risks posed by Covid-19 or from the inability of actual GDP numbers to meet elevated expectations. Meanwhile, the US 10-year Treasury yield has risen by over 100 bp since August 2020 to 1.65-1.70% and at these levels, US Treasuries offer a reasonable safe-haven hedge for portfolios.

FED EXPLICIT

The Fed has been explicit that they will allow the US economy to “run hot” and permit an inflation overshoot above their 2% target in line with their average inflation targeting policy. Nonetheless, interest rate futures markets have begun to bet on a rate hike as soon as 2022.

The Fed will need more evidence of permanence in the rise of inflation, and a closing of the output gap before it signals that a lift-off is necessary. Even so, if the Fed is intent on changing their interest rate policy, this will be clearly messaged well ahead of the event and the quantum of hikes are likely to be muted.

The risks of increasing the cost of financing before the economy has truly “escaped” from the effects of the pandemic make this a high hurdle to surpass. Nonetheless we are wary about longer-term structural inflation at some point derailing markets but that seems someway off for now.

Investors may feel increasingly concerned about the threat of inflation and see the need to react immediately. But we urge caution given the distorting base effects versus first quarter of 2020, and to await clearer data signals from consumer demand and the Fed’s reaction function.

The rise in debt globally in recent years has been government-led, largely arising from the fiscal measures needed to mitigate the economic contraction caused by the pandemic. The build-up in sovereign debt could impact the credit ratings in some EMs, such as India. Investors will have to be selective within the EMs and having the flexibility to dynamically allocate across different sectors can help investors enjoy the region’s higher yields, but with lower volatility.

Elevated government debt levels would pose a risk to growth and consequently increase defaults if inflation becomes an issue. In the face of high and sustainable inflation, significant central bank tightening would impede growth and make it challenging to service debt. However, until this comes about, the twin impact from low rates and asset purchases by the Fed and European Central Bank should be supportive of credit markets.

Corporate defaults are not expected to rise substantially in the near-term as the economic upswing lifts corporate earnings. This should in turn help contain credit spreads although active credit analysis and being selective remains key.

While default rates in the Asian High Yield bond market should remain flat or rise moderately, defaults will remain manageable. The Asian High Yield market’s attractive valuations, higher yields and shorter duration make it a compelling proposition for yield seeking investors although investors may need to ride through the current period of volatility.

Onshore bond defaults are likely to pick up in China as the government seeks to reduce net leverage in the system and reduce moral hazard in its bond market. That said, government support of state-controlled entities is likely to be assessed on a case-by-case basis, with the aim to avoid any financial systemic risks.

RESURGENT DEMAND

With ever more stimulus being discussed, and given resurgent consumer demand and robust corporate earnings, a number of risk factors could materialise to impede the current recovery. Higher debt costs at the national level as opposed to the corporate level can become an issue going forward if inflation picks up.

At the same time, a policy mis-step from central banks or governments that prematurely reverses the current supportive monetary and fiscal policy will be damaging; any tapering or reversal of stimulus must be well telegraphed and sufficiently justified.

On the corporate front, any unfavourable regulatory and tax changes in the US possibly targeting big tech and banks as per the Democrats pre-election campaign messaging needs to be monitored. Further, we think that corporates that fail to adapt their business models to the prevailing environment will be impacted.

Those corporates that were dynamic and proactive in their responses to the pandemic have reaped the rewards. ESG concerns and sustainable corporate behaviour are of paramount importance. Companies that fail to align with this change will suffer from reputational damage, weaker share prices and higher costs of financing.

- Ooi Boon Peng is Head of Eastspring Investment Strategies and Kelvin Blacklock is Head of Eastspring Portfolio Advisors