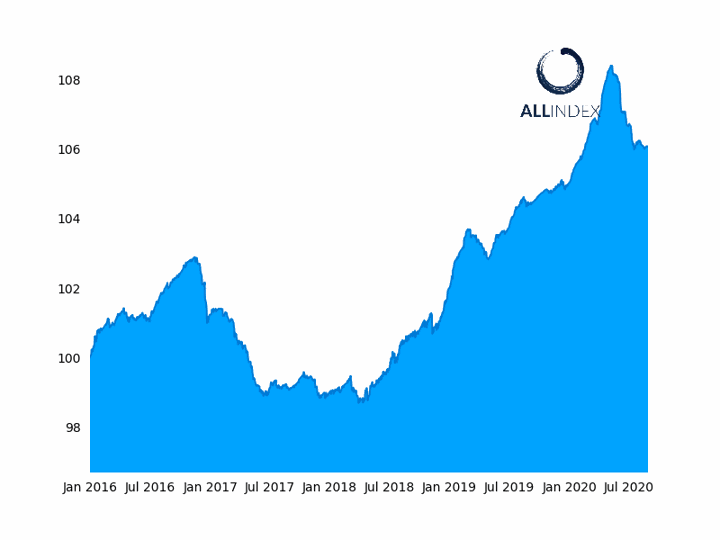

(ATF) The ATF indices closed the week stable on Friday, ahead of China’s PMI prints due next week, with the flagship China Bond 50 index, and the ATF ALLINDEX Corporates, Enterprise and Local Governments inching up 0.01%. The ATF ALLINDEX Financial didn’t move at all.

However, losses were seen in the indices with two industrial names and two financial institutions recording the biggest falls. Guangzhou Metro, a constituent of the ATF ALLINDEX Corporates, Enterprise and the China Bond 50, dropped 0.68%. Beijing Capital lost 0.45% and weighed on the ATF ALLINDEX Enterprise. China Development Bank retreated 0.22%, dragging down the China Bond 50 index and Bank of Jiangsu, a constituent of the ATF ALLINDEX Financial, fell 0.51%.

Other losses in the financial sector were recorded in the bonds of Shanghai Pudong Development Bank (-0.05%) and the Export-Import Bank of China (-0.08%), which both feature in the China Bond 50 index, and Everbright Financial Leasing (-0.02%), a constituent of the ATF ALLINDEX Financial. Shanghai Pudong Development Bank is also a constituent of the ATF ALLINDEX Financial.

The flagship China Bond 50 index rose by 0.01% on Friday.

The data prints due out next week include the manufacturing and non-manufacturing PMI scheduled for Monday 28 August, the Caixin Manufacturing PMI due on Tuesday 1 September, and the Caixin Services and Composite PMIs due on Wednesday 3 September.

Iris Pang, Chief Economist, Greater China at ING in Hong Kong expects the PMI levels to be stable and for China to post similar figures to last month. “Factory activities will still be growing, but at the same speed as last month, while the growth in services may be a little lower. However, there are activities in the services sector that could be an engine for growth in the coming months.”

The non-manufacturing PMI edged down to 54.2 in July 2020 from 54.4 in the prior month. The manufacturing PMI unexpectedly rose to 51.1 in July 2020 from 50.9 in June.

She noted that tourism within China could emerge as a highlight supporting the economy. However, other services in the insurance and financial sectors may slow a little, she added. “I am not overly concerned about this and expect that we will see positive growth still in the 3rd quarter GDP figure.”

Alicia Garcia- Herrero, Chief Economist Asia-Pacific at Natixis, echoed Mrs Pang’s views, stating that a slowing recovery is an understandable development given that manufacturing activities are normalising from the Covid-19 slump.

She projects an improvement in the manufacturing PMI for August, albeit not as strong as that of July.

“The reason for the recovery not to strengthen further might be related to persisting uncertainties about the pandemic globally and/or the still relatively poor labor market in China, which continues to suppress consumption,” she noted in a research report.

Garcia-Herrero analysed the sentiment in Chinese media in five key sub-components of the official manufacturing PMI – production, new orders, raw materials inventory, employment and supplier’s delivery time – in order to predict the upcoming PMI figure and future economic recovery.

She identified an improvement in new orders (in line with a noticeable recovery of industrial production and profits) and a slight recovery in employment and suppliers’ delivery time in August. However, the data highlighted a worsening in sentiment on production and raw material inventories.