Global investors will probably demand more protection from riskier bond issuers in China and Asia by seeking higher returns and more transparency as a result of Evergrande Group’s financial woes.

Suffocating under $305 billion in debt and teetering on the brink of collapse, property developer Evergrande missed making payments to offshore bondholders twice last month and has not announced plans yet to repay those investors.

It has another eight offshore and one onshore coupon repayments due before year end.

The failure to make payment, followed by a string of credit rating downgrades of indebted Chinese developers, has roiled China’s high-yield debt, sparked outflows and is now making asset managers jittery about issuers in the region, investors and analysts said.

Arthur Lau, Hong Kong-based PineBridge Investments’ head of Asia ex-Japan, fixed income, thinks the heady mix of debt woes and changing regulations in China is shifting goalposts for foreign investors.

“These uncertainties have caused material impact to the risk appetite for the Chinese assets,” Lau said. “A higher risk premium may warrant given the unpredictability of policy reforms at the moment.”

Signs of stress in China’s property sector are coming thick and fast – developer Fantasia Holdings failed to pay a $206 million bond due Monday and its peer Sinic Holdings suffered a ratings downgrades on Tuesday, after certain units missed interest payments on onshore financing arrangements.

Uncertainty over when and if authorities will step in to cushion the contagion risk from Evergrande at a time when Beijing’s regulatory crackdown has already frayed nerves and growth in the economy is slowing has sent bonds sharply lower.

Billions flow out of Chinese debt

Foreign investors yanked $8.1 billion out of Chinese debt in September – the largest outflow in six months – while emerging market fixed income ex-China enjoyed inflows, data from the Institute of International Finance showed.

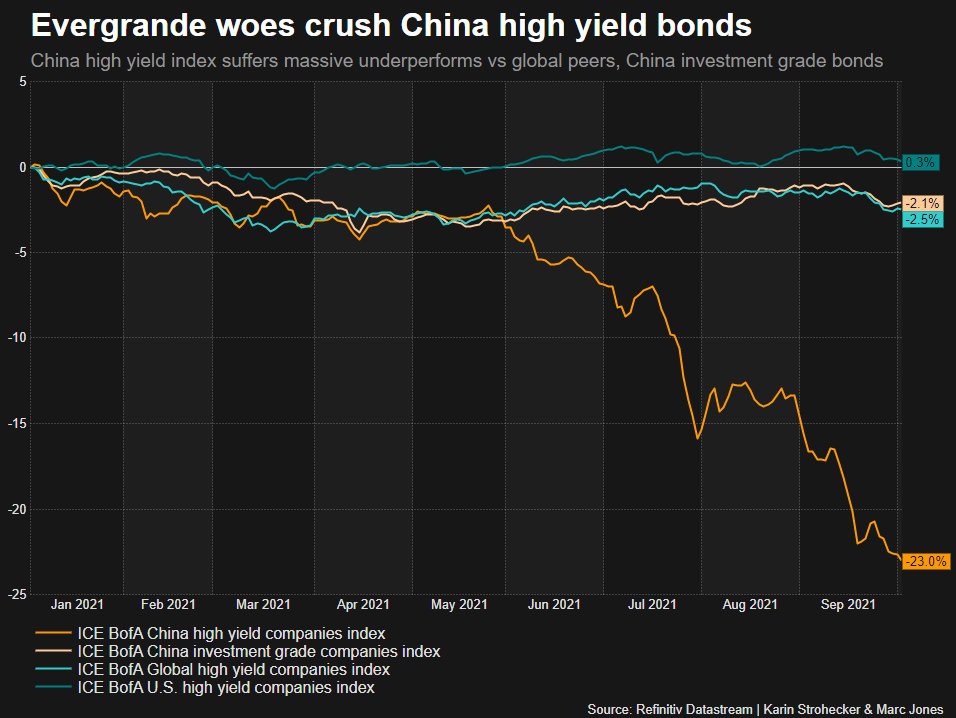

Much of the pain is concentrated in high yield firms in the country – ICE BofA’s China high yield index has lost around a quarter since the start of the year while the global benchmark and China investment grade peers barely budged.

Analysts say the sharp losses for Chinese junk bonds reflected both default risk and uncertainty over how to value bonds given the unclear picture of how Evergrande debt may be restructured and authorities’ ability to stop the spread to other firms.

Standing at 160% of gross domestic product (GDP), China’s non-financial corporate debt is higher than the advanced economy average and ratings agencies have regularly flagged asset quality as a concern, Adam Slater at Oxford Economics said.

“How much of the recent rise in risk premia prove to be permanent is as yet unclear,” he said, adding much would hinge on the success of Chinese authorities at containing financial contagion from Evergrande.

Pressure has been felt outside the property sector, too.

Bonds maturing in five years and issued by West China Cement, aluminium producer China Hongqiao Group and leasing firm Ehi Car have seen their yields jump by more than 1 percentage point since the end of August.

Wall of Maturity

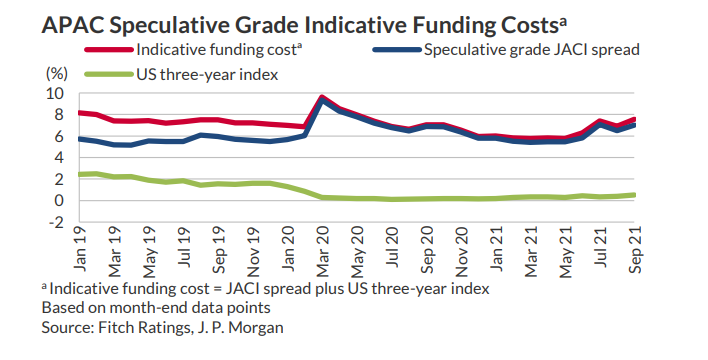

Evergrande’s reverberations are being felt beyond China. Ratings agency Fitch calculates that funding costs for Asia Pacific junk-rated corporate issuers have risen by more than 1 percentage point to 7.5% by end-September.

The 50 major Asian high-yield corporate issuers – who have $423 billion in debt outstanding between them – might enjoy a bit of breathing space for now with just $2.6 billion maturing until year-end, Fitch calculates.

But that will soon change when a record $28.2 billion comes due in 2022 followed by $28.7 billion in 2023, the ratings agency said in its latest report.

The group is dominated by China and the real estate sector, but also contains firms from India and Malaysia to Mongolia.

More Transparency and Disclosure

Analysts also predict the latest events will sharpen a push by investors for more favourable conditions.

“The lasting impact in terms of pricing might come in the form of investor insistence on improved company transparency and disclosures,” Jim Veneau, AXA Investment Management head of Asia fixed income, said.

Philip Lee, head of debt capital markets for Asia Pacific at DLA Piper, expects to see “demand for tighter covenants in bond documentation as well as greater focus on group guarantees and asset security.”

Given the sheer size of China’s bond market at $16 trillion, comparatively high yields and increasing importance in global indexes and financial markets, some bet that investors will see through the current turmoil in the near future.

This month will see the start of the inclusion of Chinese government bonds in the FTSE Russell WGBI index – a widely followed fixed income benchmark – that could see large amounts of passive investments flow into the country’s debt markets.

“In the long-term, we believe this market is simply too vast to ignore,” PineBridge’s Lau said.

• Reuters with additional editing by Jim Pollard