A stress analysis of Chinese property developers publicly rated by Fitch has highlighted potential liquidity strain for close to one-third of the portfolio under a ‘severe’ scenario involving a 30% decline in residential home sales revenue in 2022.

Such a scenario could also worsen credit polarisation among public-finance entities, as well as have flow-on impacts on related sectors, such as construction, engineering and commodities, the ratings agency said on Monday.

In its report titled ‘Cross-Sector Study: China Property Stress‘, Fitch said that tight funding access and diminished cash flow from lower property sales were driving an unprecedented liquidity crunch for Chinese developers.

“A prolonged decline in housing sales can reverberate across the value chain, as property and construction sectors directly account for around 13%-14% of China’s GDP.

“The longer the stresses on China’s property sector last, the greater the risk of a loss in consumer confidence.”

The authorities had taken steps to accelerate mortgage approvals and encourage continued bank lending to fund projects already underway.

“However, project-level cash trapped in escrow accounts are inhibiting the use of funds for debt servicing outside project companies. Escrow accounts, which comprise pre-sale deposits, typically account for 10%-30% of a developer’s cash. They are closely monitored by local regulators to ensure the use of funds for construction of projects.

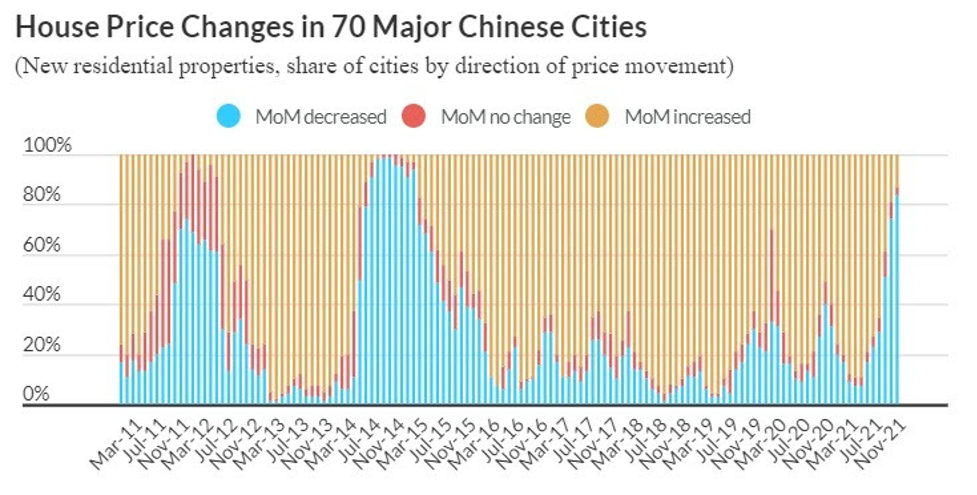

“Weak market sentiment is also affecting residential home sales, as buyers postpone purchases in anticipation of further price reduction.”

Fitch said its baseline assumption incorporates a 10-15% fall in residential property sales by value for 2022 (with 2021 flat year-on-year) – and an average selling price decline of around 5%, underscoring the group’s deteriorating sector outlook.

Three Months of Falling Sales

Residential home sales fell by 17% year-on-year in November, after declining 24% in October and 17% in September, it said.

“Price falls were steeper in lower-tier cities, where there are fewer home-buying restrictions compared with higher tier cities, where strict curbs suppressed demand. Lower-tier cities also have weaker economic fundamentals.”

Things are expected to get tougher in 2022, as most analysts say the government appears determined to try to make homes more affordable for its citizens and has shown no sign of wanting to ease lending restrictions to deeply indebted developers such as China Evergrande that exceeded the ‘three red lines’ debt limits imposed in August 2020.

In addition to a downturn in housing sales, the agency’s severe scenario envisages tight financing conditions up to June 2022, with onshore and offshore bond maturities needing to be repaid from internal resources, and some net repayment of trust loans and bank borrowing.

“Under our stress assumptions, we estimate 12 of 40 developers rated ‘B-’ or higher would experience a net cashflow deficit. Developers in the ‘B’ category are most affected. We have assumed the majority of bank borrowings and trust loans can be refinanced. However, creditor confidence can weaken swiftly, which would sharply worsen refinancing capabilities.”

Property-related sales are also an important source of funding for local and regional governments (LRGs) in China as capital revenues (mostly from sales of land-use rights) account for about 25% of their annual fiscal revenues, the agency said.

“A fall in these revenues would affect LRGs’ ability to support highly geared local-government financing vehicles.

“Our analysis finds that nine of our portfolio of 147 rated public-finance entities in China are most at risk, as they have moderate or high sector exposure to housing and balance-sheet vulnerability, while their related LRGs have weaker credit profiles and are less able to provide support.”

• Jim Pollard

ALSO SEE:

Second Ratings Agency Declares Evergrande In Default

Chinese Banks To See Jump In Bad Property Loans: S&P

China Evergrande Debt Crisis: The Next Flash Points