As China faces a growth slowdown, the technology-driven “intelligent economy” and emerging consumption trends offer protection against slackening economic activity, but more targeted government policies will still likely be needed to sustain momentum.

In the first half of the year, Beijing was on track to meet its 2025 growth target of 5%, with 5.4% and 5.2% growth recorded in the first two quarters, but activity appears to have slowed since.

This was emphasized by China’s August activity report, which highlighted the deceleration in retail sales and industrial output.

ALSO SEE: Indian Central Bank to Ease Foreign Borrowing Rules for Firms

There are, however, bright spots in China’s economy – many of which have been beneficiaries of new and ongoing government policies.

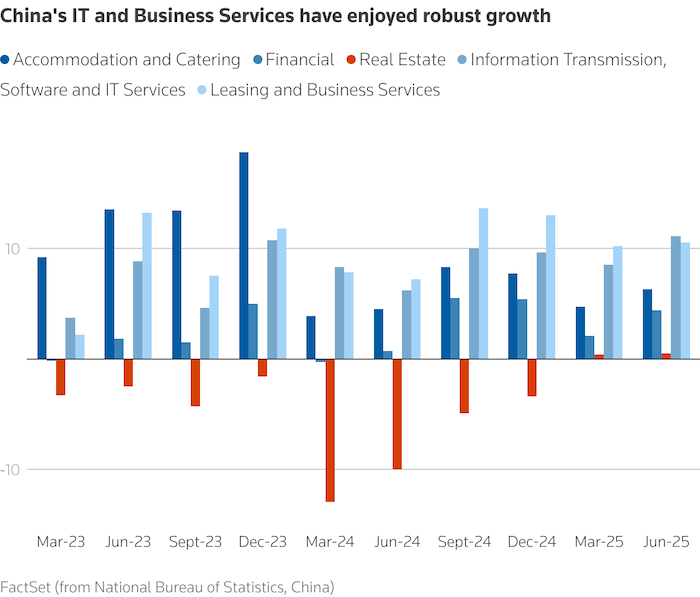

First, Beijing’s efforts to support China’s “intelligent economy” – eg, artificial intelligence, semiconductors and other advanced manufacturing – have helped the Information Technology and Business Services sectors outshine many others since early 2024.

The chart shows the growth in the components of China’s service sector GDP from the March 2023 quarter to the June 2025 quarter.

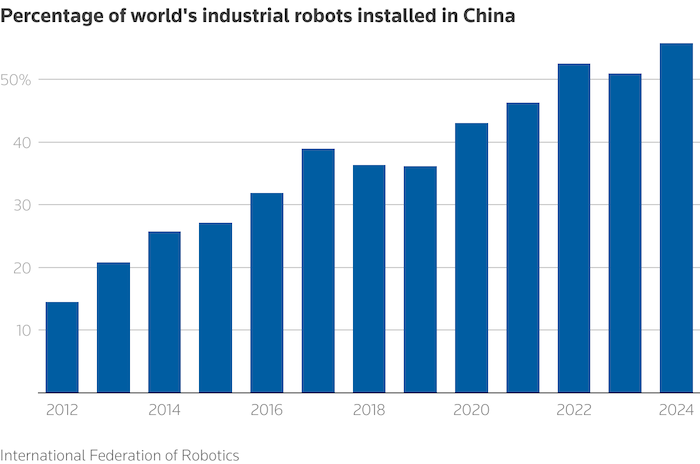

This trend looks set to continue, as China is investing massively in industrial and humanoid robots that could boost productivity. Over the last three years, more than half of the world’s industrial robots were installed in China.

This Reuters chart shows the number of industrial robots installed in China.

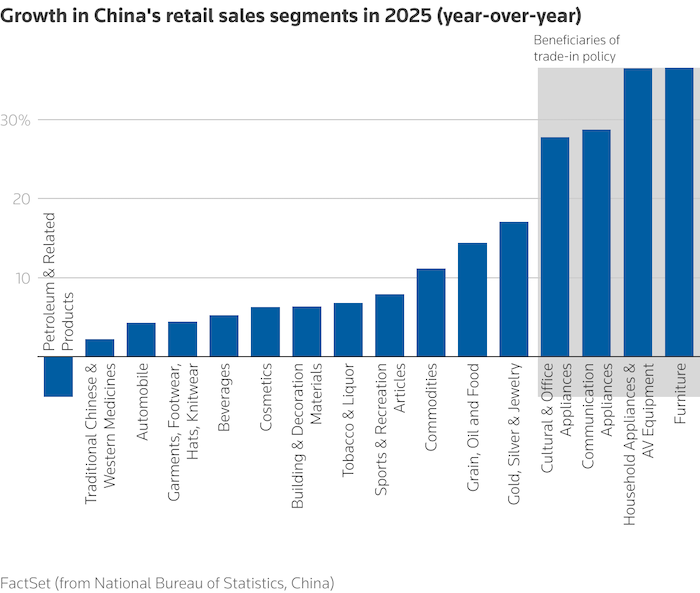

Targeted government policy also seems to have put a floor under retail sales, which grew modestly in the first eight months of 2025. Household appliances, furniture, communication and office equipment – the fastest growth segments in the retail sector – have all benefited from China’s trade-in policy instituted in late 2024.

The chart shows year-on-year growth in various segments of China’s retail sales in 2025 (till August).

Some government measures have hurt consumption as well. China’s anti-extravagance mandates for government officials, which were reaffirmed in May, have negatively impacted the restaurant, liquor and catering sectors from June onwards.

Shift in consumer preferences

Another driver of growth this year – and one that could persist moving forward – is the shift in consumer preferences.

Chinese millennials and Gen-Z are flocking to new types of domestic products and services, especially those that promote social engagement, combine tradition with modernity, and engage customers with AI and other digital technology.

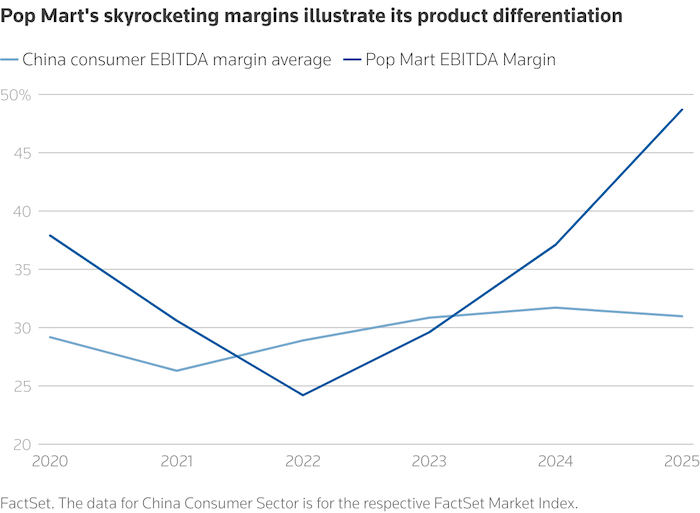

Such “new consumption” has helped drive the sales of PopMart’s Labubu doll, and has also boosted the popularity of tea house chain Chagee’s Chinese opera-inspired outlets and Laopu Gold’s jewellery rooted in traditional Chinese craftsmanship.

PopMart’s exploding margins stand out here, in part because China’s overall consumer goods sector is stagnating. This suggests that novel types of products and services in China have the potential to break out of their categories.

Chart pop mart

One could also argue that PopMart’s success is a one-off that would be difficult to replicate on a broader scale. Moreover, such astronomical growth could presage a rapid decline if the Labubu fad fades.

On the other end of the demographic spectrum, the “ageing China” narrative is also spawning new businesses, including smart home technology, elder care services, financial pension plans and specialized healthcare products.

China’s “silver economy,” with an estimated size of $1 trillion in 2024, is forecast to grow to $4 trillion by 2035, China’s State Council Information Office forecasts.

While China’s new consumption patterns and “intelligent economy” have had a positive impact on growth this year, this has not been enough to offset the negative effect of decelerating activity in the manufacturing, construction and property sectors.

Meanwhile, the growing resistance in the West to Chinese exports only underscores the need to boost domestic consumption.

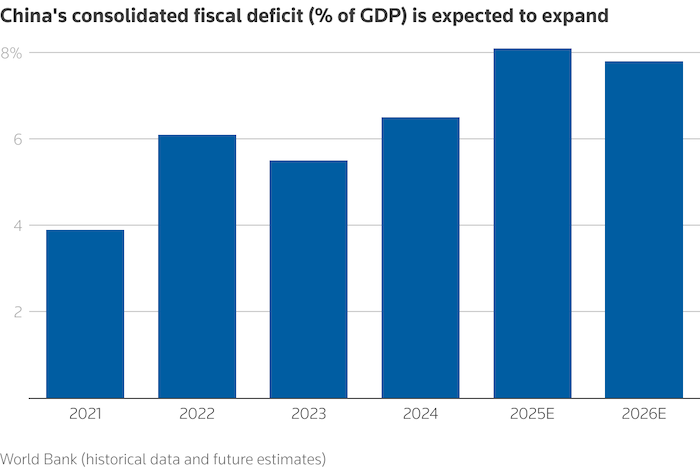

This is clearly on the government’s list of priorities, and given the country’s stubbornly low consumption sentiment, the diminishing impact of monetary stimulus and shrinking room for fiscal support, policymakers have had to expand their toolbox.

The chart shows World Bank estimates and future forecasts of China’s fiscal deficit as a percentage of GDP from 2021 to 2026.

To begin, policymakers seem to understand that consumption sentiment is unlikely to improve unless employment does.

In turn, Beijing has already started to provide targeted support to small and medium enterprises to encourage hiring. It may also seek to incentivise firms to hire with a social insurance subsidy or enhance workers’ skills through targeted vocational training.

Given that more than a third of China’s workforce are migrant workers, government policymakers have also suggested relaxing workers’ residency – or Hukou – permit requirements. This would ensure that social insurance eligibility is not tied to a registered residence, supporting consumption at the low end of the income spectrum.

Reviving the positive wealth effect could also be helpful. The flagging property sector, which accounts for 60% of the average Chinese householders’ wealth, remains a drag on consumption sentiment.

Given that the property market could take years to recover, another option may be encouraging onshore investors’ nascent interest in Chinese equities, something regulators already appear to be working on with their indirect support for a “slow bull market”.

Truly shifting to a sustainable, consumption-driven economy could be a lengthy, complex process – and pitfalls abound – but investment in advanced industries, innovation in products and services, and nimble policymaking could represent a firm foundation.

- The views expressed here are those of Manishi Raychaudhuri, founder and CEO of Emmer Capital Partners Ltd, and the former Head of Asia-Pacific Equity Research at BNP Paribas Securities.

ALSO SEE:

Chinese EV Firms Invest More Abroad Than At Home For First Time

China’s Manufacturing Slump Drags on Amid US Trade Uncertainty

EU Set to ‘Hit China With 20 Anti-Dumping Probes’ – SCMP

Trump Unveils Pharma, Truck, Furniture Tariffs: Asia Stocks Fall

Subsidies And Homegrown Tech: How China Plans To Rival Stargate

Asian Nations Queuing up to Join World’s Biggest Free Trade Bloc

Alibaba Shares Jump on Data Centre, AI Plans and the Ma Factor

China Is Full Of New Car Graveyards

Beijing Says it Will Rein in EV Sector’s ‘Irrational’ Competition